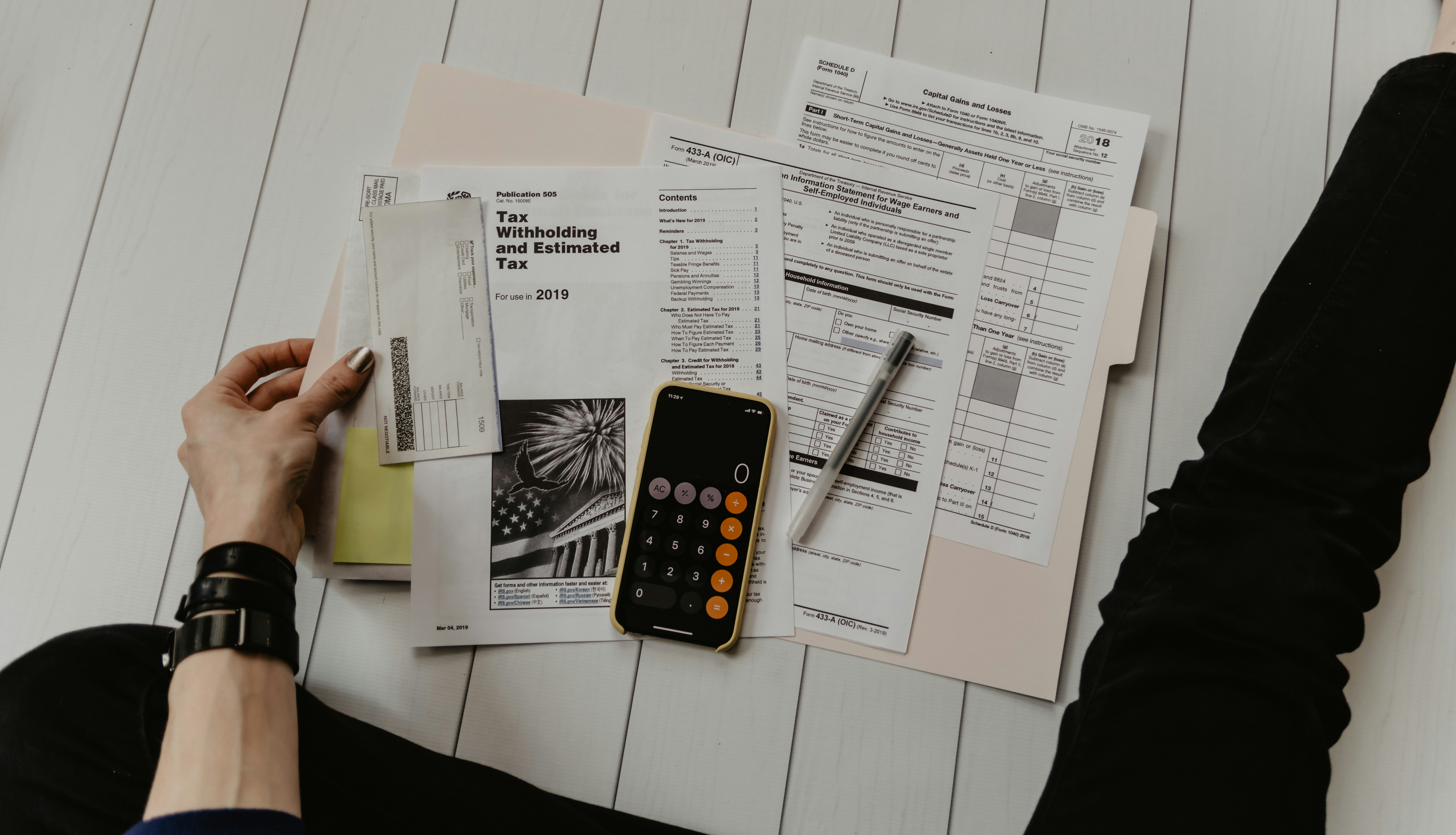

People earn and spend money on a daily basis but ironically money remains a taboo topic. Personal finance usually isn’t taught in the classroom and many adults enter the working world without knowing how to responsibly handle money. Women traditionally earn less than men in the United States and have a different approach to personal finance. Here are some essential rules and habits for women who need to develop their personal finances.

Figure Out How Much You Need to Survive

Figure out how much money you need to survive in comparison with how much you have in the bank. Build a basic budget based on your survival costs. Add up your monthly rent, utility, groceries, and transportation costs. Factor in your daily extra expenses and multiply that number by seven. Then add in any other additional bills you have and there’s your budget. What you don’t want to do is spend more than you earn each month. Any money that you have remaining at the end of the month should be transferred into a savings account.

Follow the 50-20-30 Rule

A smart personal finance habit for women to follow is the 50-20-30 Rule. Divvy up your monthly pay after taxes into three spending categories: essentials, lifestyle, and the future. 50 percent of your pay should go to your essentials, like housing, food, and utilities. 20 percent should go to a savings account or retirement fund, and the remaining 30 percent should go to your lifestyle or discretionary purchases, like entertainment, travel, and shopping.

Find Inspiring Financial Advice

Find financial success stories of other women who gained control of their finances while doing what they love. There are plenty of podcasts and finance blogs that can give you the needed inspiration to overcome your personal finance challenges.

Alastair Barnes is a financial analyst who is savvy at keeping up with the latest trends and stories in business and finance. The Fordham University alum has a flair for watching the capital market and spotting the latest happenings in business, especially with the arrival of COVID-19. Connect with Alastair Barnes to break the taboo and learn where to start the personal finance conversation.

Build a “Walk Away” Fund

Women should build a “walk away” fund that puts them in a financial power position. Also known as a rainy day fund or emergency fund, you should work towards saving up three to six months’ worth of living expenses. Losing a job, needing to leave a partner, or being liable for a large, unexpected bill could put you into a financial hole if you have to rely on credit cards for an emergency.

Most women who plan to have a family in the future don’t plan to struggle with fertility issues. Struggling to conceive and turning to IVF treatments is a logical step towards building a family. Unfortunately, IVF treatments are costly and not always covered by health insurance, meaning the financial burden falls on the patient. PFCLA can help you overcome infertility with the more cost-effective alternative mini IVF.

The mini IVF cost is lower than traditional IVF due to the use of reduced fertility medication, reduced risks, and broader candidacy. It’s an ideal option for patients who have been unsuccessful with traditional IVF and are hesitant to keep trying due to costs. If it’s time to start a family but unexpected fertility costs are in the way, consult with the specialists at PFCLA to find out what options are best for you.

Save Your $5 Bills

A simple tactic to save money for short-term goals is to stop spending your $5 bills. Every time you end up with a spare $5 bill in your wallet, take it out and put it in a money jar or piggy bank. Having a visual reminder of a savings goal will help you stay disciplined and motivated.

Use these pieces of financial advice to take control of your personal finances one step at a time.